Are you planning to finance your dream home? Understanding and comparing 30-year fixed mortgage rates is crucial for securing a mortgage that suits your financial situation. Equip yourself with the knowledge to make an informed decision by delving into the intricacies of 30-year fixed mortgage rates, the factors that affect them and the alternatives available.

30-year fixed mortgages offer stability in interest rate and lower monthly payments, though total interest paid is higher.

Factors such as credit score and down payment amount can influence mortgage rates offered by lenders.

Shopping around for the best mortgage rate and understanding APR can save borrowers thousands of dollars on their loan costs.

A 30-year fixed mortgage is a popular choice among homebuyers, offering stable interest rates and longer loan terms, which translate into predictable monthly payments. This type of mortgage allows borrowers to repay their lender over a 30-year period with a fixed interest rate that remains constant for the duration of the loan.

However, mortgage insurance may be required if the down payment is less than 20%. Numerous factors, such as the borrower’s credit score and down payment amount, as well as larger external forces, influence the mortgage rates offered by lenders.

One of the main advantages of a 30-year fixed mortgage is the stability of its interest rate. Unlike adjustable-rate mortgages (ARMs), which have interest rates that may vary over time, fixed-rate mortgages provide borrowers with a consistent interest rate for the life of the loan.

Having a constant interest rate translates into predictable monthly payments, allowing borrowers to budget and plan their finances more effectively. This is particularly beneficial for those with a long-term financial outlook, as they can have peace of mind knowing their mortgage payments will remain unchanged throughout the loan term.

The 30-year fixed rate mortgage term is another reason for the popularity of fixed-rate mortgages. Spreading the loan over a longer period results in lower monthly payments compared to shorter-term loans. This makes 30-year fixed mortgages more affordable for many borrowers, especially those with a restricted budget or who prefer to save money while making mortgage payments concurrently.

Keep in mind, the extended loan term increases the overall interest paid. Borrowers should carefully weigh the benefits of lower monthly payments against the potential drawbacks, such as higher total interest paid over the life of the loan.

When searching for the best 30-year fixed mortgage, it’s crucial to take into account factors that influence mortgage rates. These factors include:

Credit scores

Home location

Home price and loan amount

Inflation

The rate of economic growth

Federal Reserve monetary policy

The bond market

Housing market conditions

Loan-to-value ratio

Debt-to-income ratio

Next, we’ll examine the impact of credit scores and down payments on mortgage rates.

A borrower’s credit score plays a significant role in determining the mortgage rate they are offered. Higher credit scores are viewed as less risky by lenders, which can result in a lower mortgage rate. Generally, borrowers with a credit score of 740 and above are offered the most advantageous offers for a 30-year fixed mortgage.

Improving your credit score before applying for a mortgage can be a valuable strategy to secure a lower interest rate. Paying bills on time, reducing credit card balances, and limiting the number of credit inquiries are some ways to improve your credit score and qualify for better mortgage rates.

Another factor that can influence mortgage rates is the size of the down payment. Larger down payments can lead to lower mortgage rates, as they reduce the lender’s risk and the loan-to-value ratio. It is recommended that a 20 percent down payment be made for a 30-year fixed mortgage, although it is not mandatory.

Paying a larger percentage of the home’s price upfront decreases the amount borrowed and makes the borrower appear less risky to lenders, potentially leading to a lower mortgage rate. Borrowers with a higher down payment may also avoid the need for mortgage insurance, further reducing their overall borrowing costs.

To find the best 30-year fixed mortgage rates, it’s important to compare loan offers from various lenders and comprehend the annual percentage rate (APR). Shopping around and comprehending APR can help you identify the most competitive 30-year fixed mortgage rates, ensuring you make the most informed decision. You can contact our preferred lender here.

Comparing loan offers from multiple lenders is vital in securing a competitive rate for a 30-year fixed mortgage. This can be done by:

Contacting lenders both online and over the phone

Asking for personalized rate quotes based on your credit profile

Comparing the offers to find the best fit

Keep in mind that even a 0.1 percent variation in interest rate can result in thousands of dollars paid over the duration of the loan.

In addition to comparing offers from various mortgage lenders, you can also consult a mortgage broker who will shop around on your behalf or seek advice from financial experts at your current bank or a housing counseling organization to gain insight on how to improve your credit score and secure a competitive rate for a 30-year fixed mortgage.

The annual percentage rate (APR) is a crucial factor to consider when comparing mortgage offers. It encompasses the interest rate plus other fees and charges associated with the loan, providing a more comprehensive view of the overall borrowing cost.

When comparing loan offers, it is important to look at both the interest rate and the APR, as the APR can give you a better idea of the total cost of the loan. This can help you make an informed decision when choosing a mortgage lender and ensure you are getting the best deal possible for your 30-year fixed mortgage.

For an informed decision, it’s necessary to balance the advantages and disadvantages of a 30-year fixed mortgage. The main advantage is lower monthly payments due to the extended loan term, making it more affordable for many borrowers. However, the primary drawback is the higher total interest paid over the life of the loan. Let’s examine these aspects in more detail.

The lower monthly payments of a 30-year fixed mortgage are one of its main attractions. By spreading the loan over a longer period, borrowers can enjoy smaller monthly payments compared to shorter-term loans, such as 15-year or 20-year mortgages.

Lower monthly payments can make homeownership more accessible, especially for those with a restricted budget. This allows borrowers to manage their monthly expenses more effectively and potentially allocate more funds towards savings or other financial goals, such as homeowners insurance, thanks to programs like the Federal Housing Administration.

On the flip side, the longer loan term of a 30-year fixed mortgage also leads to higher total interest paid over the life of the loan. While the lower monthly payments may be more affordable, the extended term means that borrowers will pay more in interest over time.

This trade-off between lower monthly payment and higher total interest paid should be carefully considered before deciding on a 30-year fixed mortgage. Borrowers should evaluate their financial goals and priorities, as well as their ability to afford higher monthly payments if they opt for a shorter-term loan.

Although 30-year fixed mortgages are a common choice, exploring alternative mortgage options that could better fit your financial needs is advisable.

Adjustable-rate mortgages (ARMs) and shorter-term fixed-rate mortgages are some alternatives worth considering.

Adjustable-rate mortgages (ARMs) are loans with an interest rate that may change periodically throughout the loan term, based on fluctuations in an index, such as the U.S. The New York Fed publishes Treasury-Index (T-Bill) and the Secured Overnight Financing Rate (SOFR) daily. These rates are widely used in financial markets.

ARMs typically offer lower initial interest rates compared to fixed-rate mortgages, which can result in lower monthly payments during the initial fixed-rate period. However, the interest rate may increase or decrease after the initial fixed-rate period, making monthly payments less predictable.

Borrowers considering ARMs should weigh the potential benefits of lower initial rates against the risk of fluctuating interest rates.

Shorter-term fixed mortgages, such as 15-year or 20-year loans, offer lower interest rates but higher monthly payments compared to 30-year fixed mortgages. These loans enable borrowers to pay off their mortgage faster and save on total interest payments over the life of the loan.

However, the higher monthly payments associated with shorter-term fixed mortgages may not be feasible for all borrowers. Before choosing a shorter-term fixed mortgage, it’s crucial to evaluate your financial situation and determine whether you can comfortably afford the higher monthly payments.

Mortgage points, also known as discount points, can help lower the interest rate on a loan. Understanding how mortgage points work and calculating the break-even point can help you decide whether buying points is a wise financial decision.

Understanding how mortgage points work is important when deciding whether to buy them. Mortgage points are mortgage points.

Mortgage points are fees that a borrower pays to a lender in exchange for a reduced interest rate on a mortgage loan. Generally, each point costs 1% of the total loan amount and can reduce the interest rate by one-eighth to one-quarter of a percent.

Purchasing points may reduce the interest rate on a loan, leading to reduced monthly payments and an overall reduction in the cost of the loan. However, the benefits of purchasing points should be weighed against the initial cost, which may not be feasible for certain borrowers, as well as the likelihood of remaining in the loan long enough to recoup the cost of the points.

The break-even point is the point at which the cost of purchasing mortgage points is equivalent to the savings derived from a reduced interest rate. To determine the break-even point, divide the cost of the mortgage points by the monthly savings from the lower interest rate.

For example, if the cost of the mortgage points amounts to $2,000 and the monthly savings from the lower interest rate is $50, the break-even point would be 40 months. Knowing the break-even point can help you decide whether purchasing mortgage points is a financially sound decision.

Refinancing a 30-year fixed mortgage can be a strategic move to lower interest rates or change loan terms. Before refinancing, it’s essential to consider the potential benefits and drawbacks, such as closing costs and the impact on your overall financial situation. Refinancing can be an effective way to save money.

Refinancing a 30-year fixed mortgage can result in lower interest rates, potentially saving money over the life of the loan. By capitalizing on lower market rates or switching to a different loan product, borrowers can:

Reduce the amount of interest they pay over the loan term

Lower their monthly mortgage payments

Shorten the length of their loan term

Access equity in their home for other financial needs

However, it’s important to consider the closing costs associated with refinancing, such as lender’s fees, an appraisal and other related expenses. Weighing the potential savings from lower interest rates against the costs of refinancing will help you determine whether refinancing is a financially beneficial decision. Myself or our preferred lender can tell you how to offset refinancing closing cost.

Refinancing can also allow borrowers to change their loan terms, such as switching from a 30-year fixed mortgage to a 15-year fixed mortgage or an adjustable-rate mortgage (ARM). Changing loan terms can offer benefits like lower interest rates and faster loan repayment, but also may result in higher monthly payments.

To decide whether changing loan terms is the right move, consider your financial goals, priorities and ability to afford higher monthly payments. Assessing your financial situation and understanding the implications of changing loan terms can help you make an informed decision.

Before embarking on a 30-year mortgage application, it’s advisable to enhance your credit score and compile the necessary documentation. Doing so can increase your chances of securing the best mortgage rates and terms for your financial situation.

Improving your credit score is an important step in preparing for a mortgage application. A higher credit score can increase your chances of securing a competitive interest rate and favorable loan terms.

To improve your credit score, consider the following strategies:

Pay bills on time

Reduce credit card balances

Limit the number of credit inquiries

Regularly check your credit reports for errors and dispute any inaccuracies

Implementing these strategies can help improve your credit score.

Gathering the required documentation is another critical step in preparing for a 30-year mortgage application. Lenders typically require the following documents:

Personal identification

Proof of income

Tax returns

Bank statements

Assets and debts information

Home appraisal report

Having these documents ready and organized before applying for a mortgage can help streamline the application process and increase your chances of approval. Ensuring that all required documentation is accurate and up-to-date can also help you avoid any delays or roadblocks during the mortgage application process.

In conclusion, understanding and comparing 30-year fixed mortgage rates is essential for securing a loan that fits your financial situation. By considering factors such as interest rate stability, loan term length, credit scores and down payments you can make an informed decision about your mortgage. Additionally, exploring alternative mortgage options, understanding the implications of mortgage points and discounts, and preparing for the mortgage application process can help you achieve the best possible outcome in your homeownership journey.

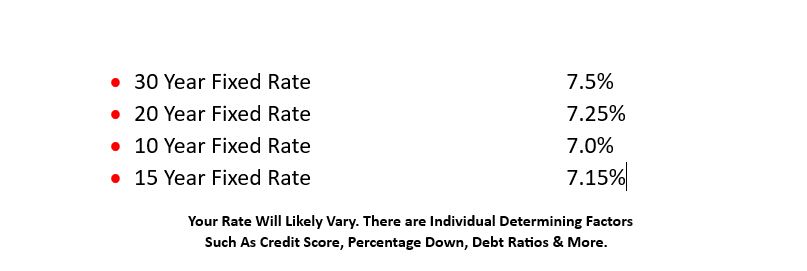

The current rate for a 30-year fixed mortgage is 7.12%, as of this week.

This average rate has been consistent over the last 90 days, with an average rate of 7.69%.

Current interest rates for 30-year and 15-year fixed-rate mortgages stand at 7.23% and 6.55%, respectively, with both seeing increases of 0.14 and 0.09 percentage points from a week ago.

These increases are the result of a strong economy and rising inflation, which have caused the Federal Reserve to raise interest rates. This has led to higher mortgage rates, making it more expensive for potential homebuyers to purchase a home.

It appears that mortgage interest rates will likely decrease in 2024, with predictions ranging from 6% to 6.7%.

This could be a great opportunity for those looking to purchase a home or refinance their current mortgage. It could also be beneficial for those who are looking to invest in real estate.

It is important that it is important.

The lowest recorded 30-year fixed mortgage rate was 2.65% in January 2021, a dramatic drop from the 8% long-term average which could be attributed to the effects of COVID-19.

This would mean an annual savings of $7,900 for a $200,000 loan.

Currently, the 30-year mortgage rate is 7.023%, an increase of 0.14 percentage points from a week ago.

This rate is significantly higher than last year’s average of 5.55%.

Previous Article

Next Article

407-575-5392

Wendy Morris LLC

DBA Wendy Morris Realty

Licensed in the State of Florida

BK 3146762

16797 Broadwater Avenue

Winter Garden, Florida 34787